The ultimate Banking as a Service (BaaS) overview

data-pm-slice=”1 1 []”>

Introduction to BaaS

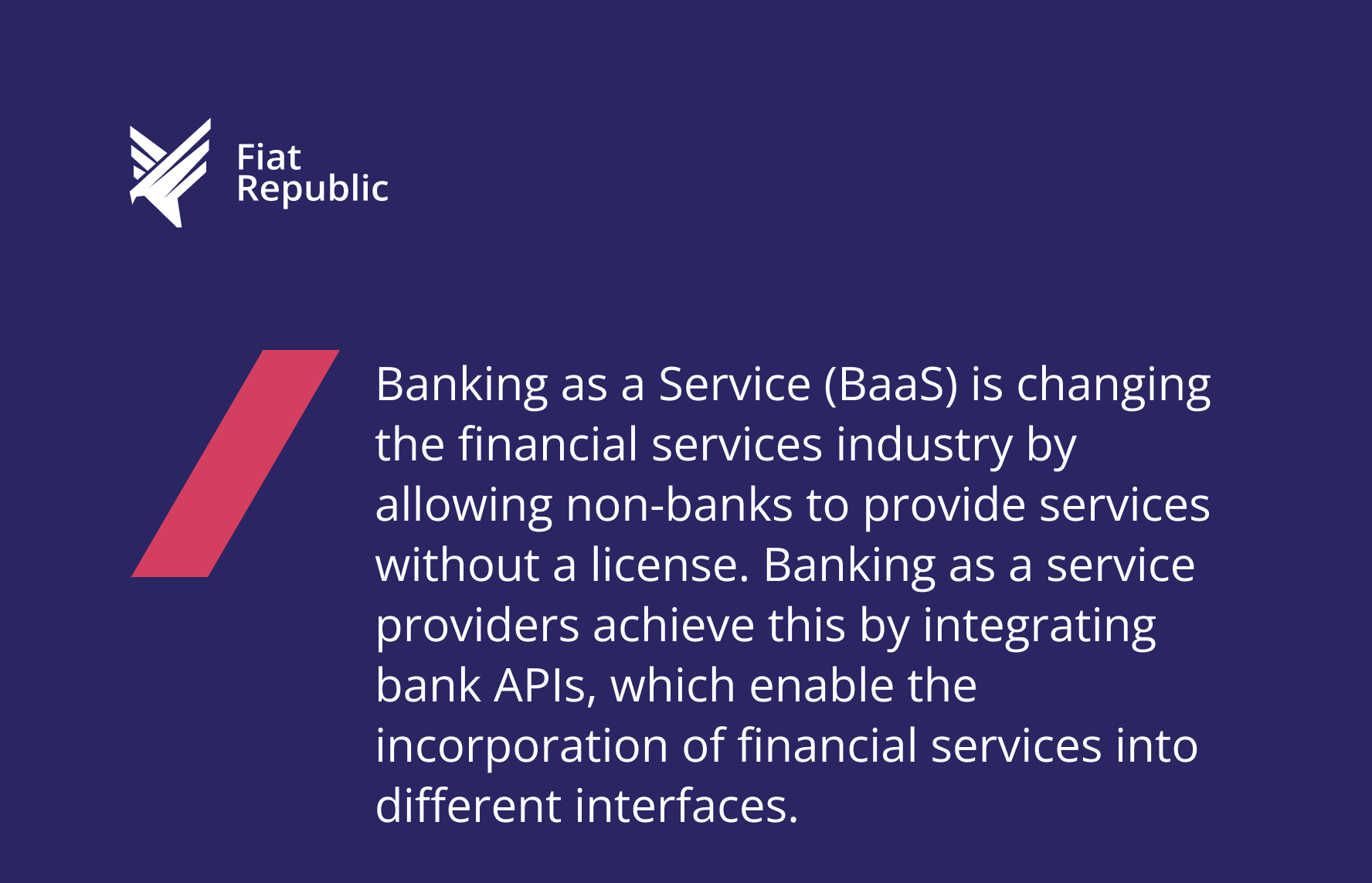

Banking as a Service (BaaS) is changing the financial services industry by allowing non-banks to provide services without a license. Banking as a service providers achieve this by integrating bank APIs, which enable the incorporation of financial services into different interfaces.

Holding a banking license is crucial for businesses offering banking services. It ensures compliance with strict regulations and capital requirements that govern financial institutions, which can be a significant barrier for non-bank entities.

BaaS has emerged as important in the modern world of financial services in several ways. It facilitates fast innovation, opens the market for new fintech players, and helps legacy banks diversify their services. The key players in the BaaS ecosystem include:

a) Traditional banks

b) Specialized BaaS providers

c) Fintech companies

d) Cloud services

e) Software providers

f) Regulatory technology firms

g) Financial institutions

What does Banking as a Service (BaaS) mean?

BaaS is a comprehensive model with several main components:

- Core banking: the fundamental systems that handle banking operations

- API: Interfaces that enable secure interconnectivity of different software programs.

- Regulatory compliance: Legal requirements for all the services provided to the public.

- Payment systems: Structures for dealing with various types of financial transactions.

- Data management and analytics: Programs for managing and processing big amounts of financial data.

- Security: Safe ways to protect any of the monetary information.

- Integration capabilities: It should be easy to integrate with different systems, referred to as integration capabilities.

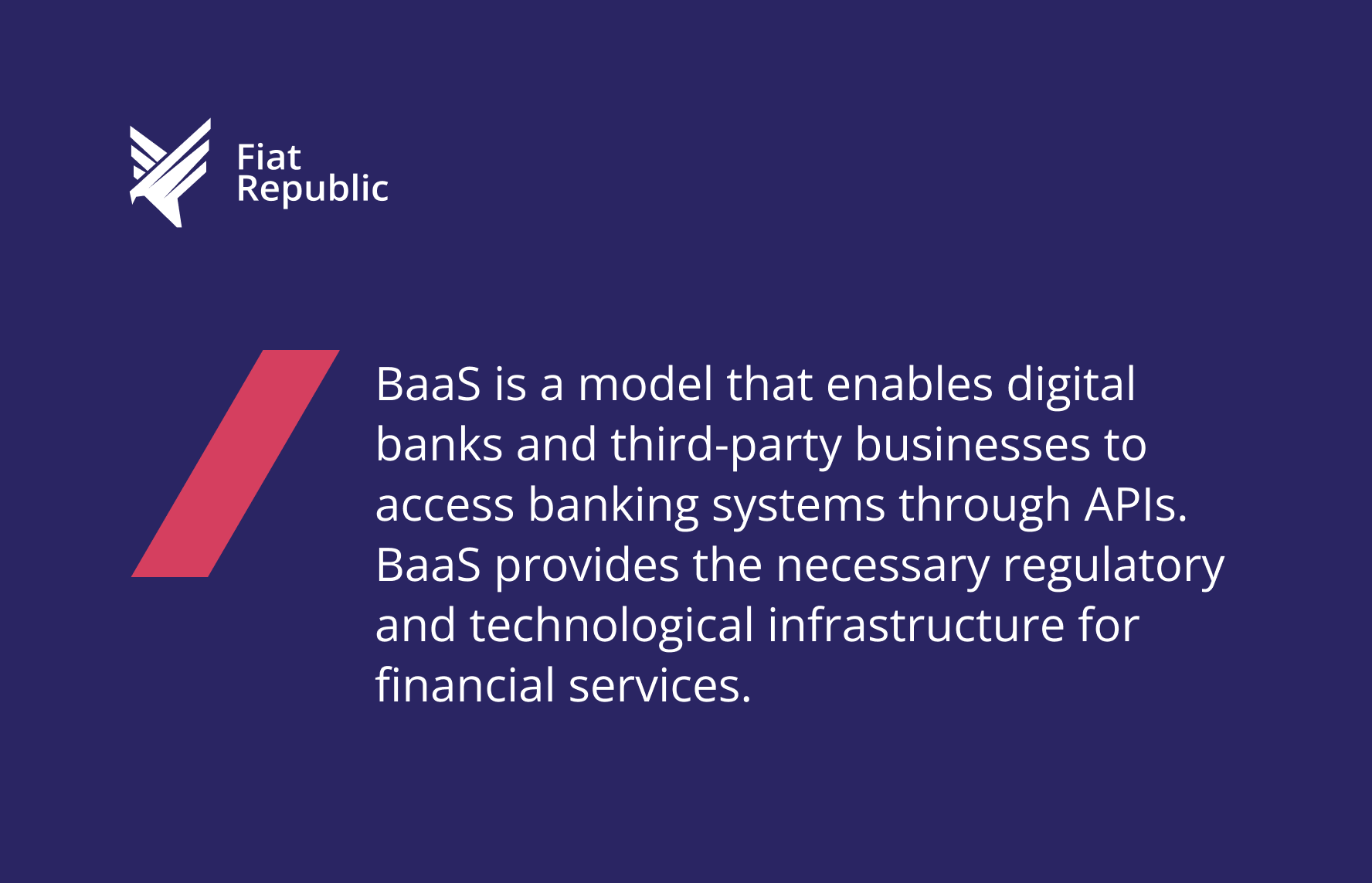

Banking as a service is a model that enables digital banks and third-party businesses to access banking systems through APIs. BaaS provides the necessary regulatory and technological infrastructure for financial services, while embedded finance refers to integrating these services into applications, emphasizing their interconnected yet distinct roles in delivering user-facing financial interactions.

In comparison to traditional banking, BaaS offers several distinct advantages.

Characteristics of BaaS:

– Offers some services that are variable and created on the premise of the Application Programming Interfaces (APIs).

– Allows other participants in the economy other than the banks to offer banking services

– Usually has lower overhead costs

– Provides more open and customer-centered banking services

– It can be market-oriented to a particular market segment or a particular market.

Characteristics of traditional banking:

– It provides all the banking services without the interference of other parties.

– Unlike the cloud, it has its physical infrastructure and depends on the internet.

– Has manually installed its core banking systems.

– It often has higher overhead expenses than the other methods of production.

– The management of introducing new products is time-consuming.

– Serves more clients with similar services

The Mechanics of BaaS

The technology used in BaaS platforms is complex. It includes robust cloud computing environments, superior API management tools, and secure data-safeguarding services. This infrastructure allows the provision of banking services in connection with non-banking services, which creates new opportunities for the development of various sectors of the economy.

However, embedding financial services directly through traditional financial institutions presents challenges such as slow digital transformation, technological shortcomings, and regulatory hurdles hindering innovation and the user experience when navigating the fragmented payments landscape.

In BaaS systems, data communication is done through API calls, where data is encrypted at least twice before being transmitted. Further, financial institutions are crucial in providing access to APIs and supporting the regulatory framework. A strict authentication process ensures that the financial data is not exposed. These systems often have elaborate anti-fraud measures and constant surveillance to enhance protection.

How does BaaS work?

A typical BaaS transaction follows these steps:

- A customer engages with an application or a service of a non-bank player.

- The customer starts a banking service request (such as opening an account or making a payment) via the app.

- This request is made through API to the BaaS provider.

- The BaaS provider goes through the request in its system.

- The result is then passed through the API back to the non-bank application that requested the check.

- The customer gets the outcome of their request as displayed in the app.

Non-bank businesses can enhance their offerings by providing payment services, allowing them to offer their customers banking functionalities without needing a banking license.

API integration and third-party access are crucial aspects of BaaS.

– BaaS providers provide several APIs for different banking operations.

– These APIs are embedded in the products that non-banks decide to provide.

– APIs can perform different tasks, such as data access, authentication, and making service requests.

– Sandbox is usually available to third-party developers, enabling them to perform integration tests before the launch.

Examples of Banking as a Service Providers

BaaS has allowed players in other industries to offer banking services to their clients. Here are some notable examples:

E-commerce solutions:

– Shopify Balance offers its users merchant banking accounts and cards.

– Amazon’s selling partners can offer credit services from the company. BaaS has evolved the financial landscape for SMBs, enabling platforms to provide tailored financial services that meet these businesses’ specific needs.

Digital banks:

– Revolut and Monzo are among the companies that offer many money services, investments, and, in some cases, cryptocurrencies. Digital banks are usually more cost-effective and have better and easier-to-use interfaces than traditional ones. Platform banking, where banks integrate services from fintech companies to enhance their offerings, differs from BaaS as it allows banks to maintain customer ownership while incorporating third-party fintech services.

Cryptocurrency exchanges with fiat capabilities:

– Most exchanges today offer the on-ramp and off-ramp through fiat currencies.

– Some exchanges even offer debit card services, making it even more difficult to distinguish between banking and crypto services.

The Impact of BaaS on Traditional Financial Institutions

BaaS is disrupting traditional banking in a very big way:

Unbundling of services:

– Customers can now select specific banking services rather than receive services from a specific institution.

– This approach is useful since it allows for developing more targeted banking experiences.

Increased competition:

– Traditional banking organizations are now facing competitive threats from entrant firms within and outside the financial industry.

– This has led many traditional banks to re-strategize their core banking offerings and enhance their digital solutions.

Revenue changes:

– API monetization and partnerships are gradually becoming new sources of revenue for banks.

– However, banks may not have a direct customer interface in many cases, which can affect customer retention and the selling of other products.

Infrastructure challenges:

– Embedding financial services often involves working with traditional financial institutions, which struggle with digital transformation and outdated technology, leading to slow processes and regulatory complexities.

– Some banks have called for API integration, which has required replacing old systems.

– Integrating agile development processes to respond to fintech developments is crucial.

Future Trends in Banking as a Service

Several trends are shaping the future of BaaS:

Increased adoption of embedded finance:

– More non-banking businesses should incorporate open banking services into their products and offerings.

– This could result in financial services being embedded in several aspects of consumers’ lives.

Growth of “invisible banking”:

– Financial services are predicted to become invisible and integrated into other aspects of consumers’ lives, making banking processes less apparent yet more ubiquitous.

Increased regulation:

– With the rise of Banking as a Service and embedded finance, it is possible to predict the appearance of new rules designed for these services.

– The emergence of ‘regulatory APIs’ might help regulate certain compliance processes.

Conclusion

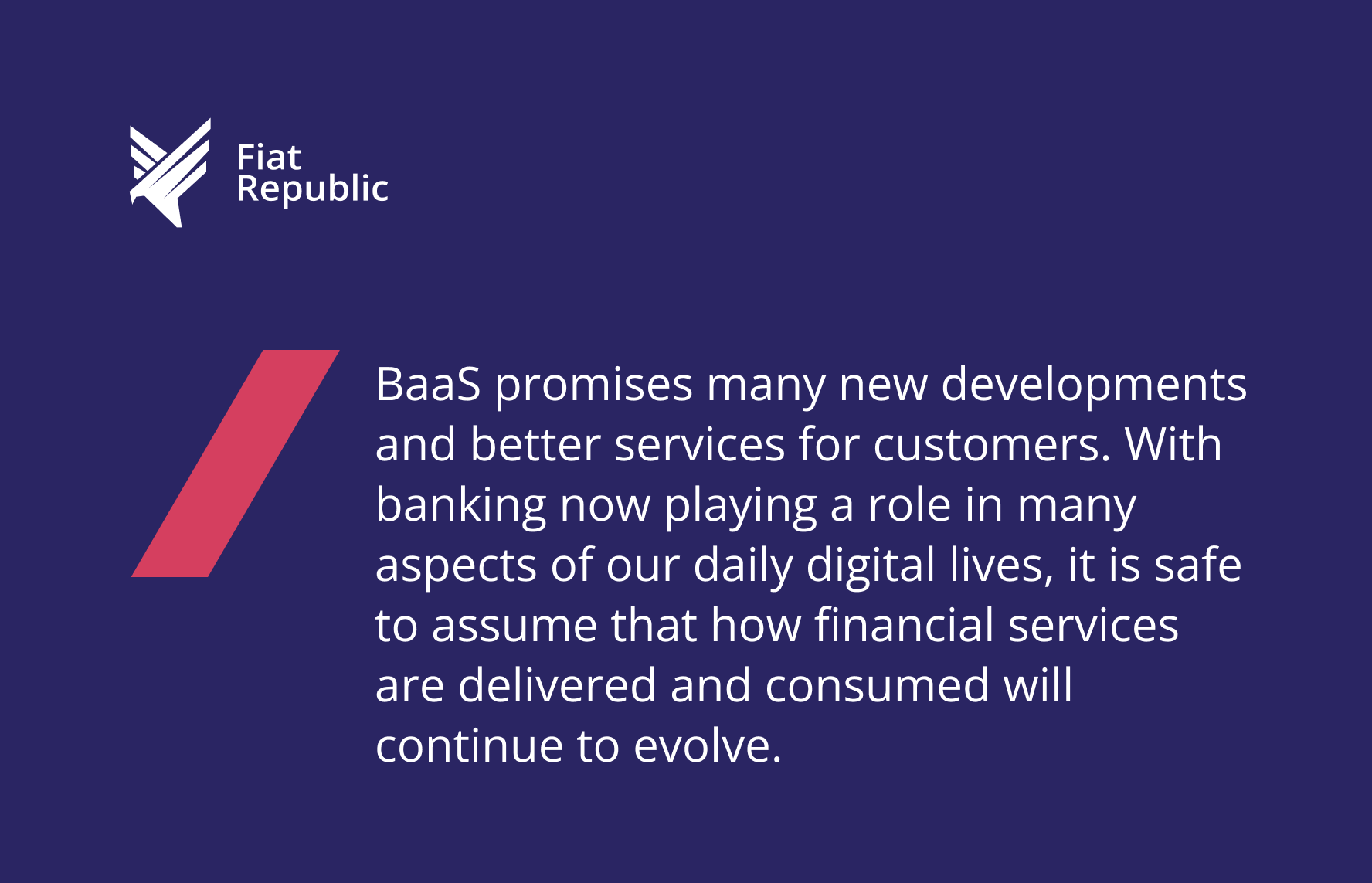

Banking as a Service promises many new developments and better services for customers. With banking now playing a role in many aspects of our daily digital lives, it is safe to assume that how financial services are delivered and consumed will continue to evolve.

In the future, conventional banks, emerging fintech players, and policymakers will need to respond appropriately to this change to build a sound, secure, and open financial system.

FAQ

What is an example of Banking as a Service?

An example of BaaS is when a fintech company offers payment cards or loan products using a traditional bank’s infrastructure. Companies like Chime and Revolut use BaaS to provide banking services without being banks themselves.

What is the concept of Banking as a Service?

Banking as a Service is a model where licensed banks integrate their digital banking services directly into other non-bank businesses’ offerings. It allows non-financial companies to offer banking services without needing to acquire a banking license.

How does a BaaS work?

BaaS works by banks opening up their APIs (Application Programming Interfaces) to third parties. These third parties can then integrate banking functionality into their products and services, leveraging the bank’s regulated infrastructure.

What is the purpose of BaaS?

The purpose of BaaS is to allow non-bank entities to offer financial services without the need to become a bank. It enables innovative fintech solutions and embedded finance, where banking services are integrated into non-financial products and services.

Why is BaaS popular?

BaaS is popular because it lowers barriers to entry in financial services, fostering innovation and competition. It also allows companies to enhance their customer experience by integrating financial services directly into their products.